The 2026/27 tax year is just a few months old. However, some significant tax changes are being brought in from April 2027, and it’s important to understand whether they might impact your personal finances.

Read on to find out about three upcoming tax changes, what they could mean for you, and how to mitigate any liability where possible.

Preparation is key to factoring tax changes into your financial plan

When the chancellor announces new financial legislation, there is usually a period of time before any changes are implemented. Aside from emergency measures which need to come into force almost instantly, changes usually take effect at the start of a tax year.

This period of grace also serves as a good time for you to assess your personal wealth and how your financial strategy may need to be tweaked in light of the changes.

While you may take notice when Budget changes are announced, this lead-in time can also mean that what was headline news is almost forgotten by the time the changes are actually implemented.

At Fingerprint, we always keep you up to date with what lies ahead to make sure that we’re optimising your financial plan in line with current and imminent legislation.

With this in mind, here are three significant changes coming into force in April 2027 that you need to be aware of.

1. Pensions included in an estate for Inheritance Tax (IHT) purposes

Pensions have traditionally acted as a fairly simple tax-efficient asset, with the added bonus that they lie outside your estate. However, from April 2027, any unused pension funds and death benefits will be brought into the scope of IHT. This could result in an unexpected bill or a higher bill than would have previously applied.

According to government estimates, 10,500 estates will have an IHT liability where they previously would not, and 38,500 will pay more than they would have before the new rules. The average IHT liability is expected to increase by around £34,000.

This means that, in some instances, it might be a case of “back to basics” for your pension, shifting it from being a tax-efficient wealth transfer mechanism back to its original purpose of funding your retirement.

There are also some strategies we can help you put in place to keep your estate out of the scope of IHT. The threshold is set at £325,000 until 2031, meaning assets above this amount will usually have IHT applied at 40%. Mitigation approaches include:

- Leaving your house to your direct descendants, which can raise your threshold to £500,000 using the residence nil-rate band

- Gifting up to £3,000 a year using the annual exemption, which is allowable without IHT being applied

- Making small gifts of up to £250 to any number of individuals

- Gifting from surplus income: these must be regular payments which don’t have any detriment to your lifestyle

- Leaving 10% or more of your estate to charity, which could reduce your loved ones’ IHT rate to 40%.

However, there could be other implications attached to these strategies, so it’s important to take financial advice before you proceed to make sure you’re operating on the most tax-efficient basis.

2. Cash ISA limits

Currently, you have a total ISA allowance of £20,000 that can be spread across a range of ISA products, which can earn tax-free interest and tax-efficient growth. From April 2027, however, while the total allowance remains the same, if you’re under 65, your allocation options will change.

You will still be able to save into a Cash ISA, but up to a limit of £12,000. The remaining £8,000 will need to be put into a Stocks & Shares ISA or a Lifetime ISA (LISA) if you plan to use your full allowance.

You can invest as much of your allowance as you like in a Stocks and Shares ISA or a LISA (up to the relevant subscription limits for each product), and the rules for Cash ISAs won’t apply if you’re over 65.

Existing balances can continue to earn tax-free interest, so if you want to boost your Cash ISA, make sure you’re using as much of your 2026/27 allowance as possible before the restrictions kick in.

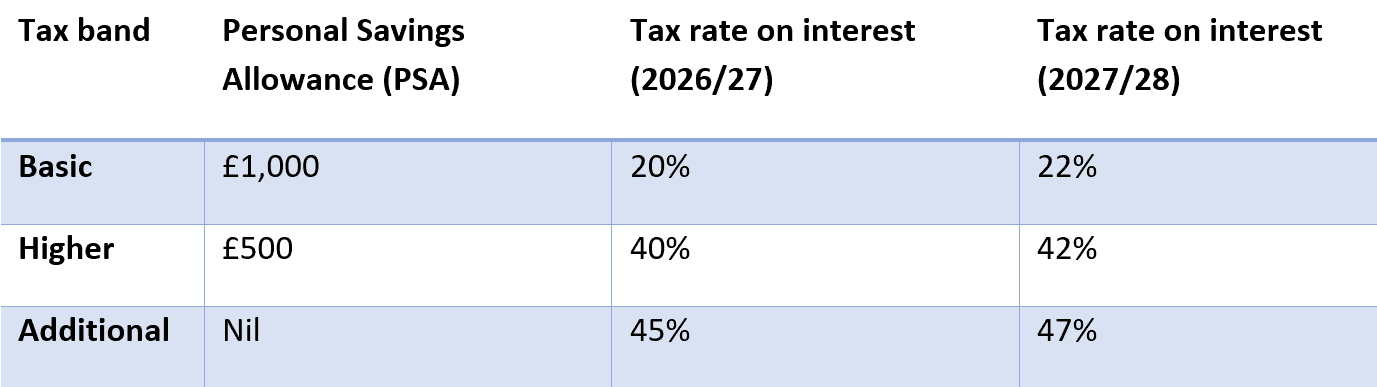

3. Income Tax rates on savings interest to rise

From April 2027, any interest you earn from either savings or property rental income will be taxed at two percentage points higher than the current rate.

Basic-rate and higher-rate taxpayers have a Personal Savings Allowance (PSA) of tax-free interest. Above is an outline of what the current PSA and tax rates on interest are and the new rates from April 2027.

Get in touch

If you’d like to find out more about how these tax changes could affect you, we’re here to help. Please get in touch by emailing hello@fingerprintfp.co.uk or calling 03452 100 100.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up, and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

The Financial Conduct Authority does not regulate tax planning or NS&I products.